S&P 500 earnings were expected to be strong and turned out to be phenomenal. When the final 5% of companies report, first quarter earnings are expected to have increased 51.9%. When the quarter began, earnings growth was expected to be less than 25%. Strong earnings from consumer discretionary companies, financials, and the communication services sector all supported rapid earnings growth.

Key Points for the Week

- S&P 500 earnings are poised to increase more than 50% based on actual results from 95% of companies in the index.

- Initial jobless claims dropped another 34,000 to 444,000, and governors in 21 states have announced they will withdraw from the federal unemployment program that pays an additional $300 per week.

- Existing home sales dipped to 5.85 million as price increases appear to be slowing sales.

Initial unemployment claims aren’t showing the same progress as earnings, but they are sliding lower. Last week, 444,000 people claimed initial unemployment. While high relative to pre-COVID data, it represents a new post-COVID low. Twenty-one states have announced they will be eliminating the enhanced unemployment benefit from the federal government as business continue to report challenges keeping up with a surge in demand.

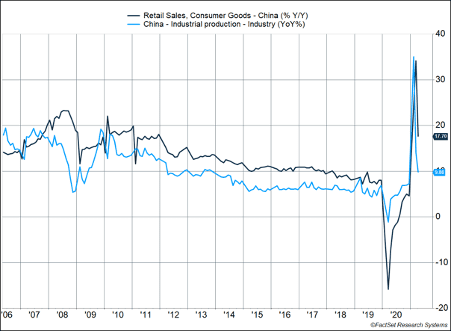

Two formerly fast-growing economic segments slowed down. In the U.S., existing home sales fell to 5.85 million last month as increasing prices and scarce supply are slowing sales. China’s retail sales increased 17.7%, and industrial production rose 9.8% (Figure 1). Both numbers missed expectations and indicate China’s economy isn’t bouncing back as quickly as some expected.

Markets calmed after several days of volatility. The S&P 500 edged 0.4% lower last week. The MSCI ACWI index gained 0.4%. The Bloomberg BarCap Aggregate Bond Index recouped 0.1% of the previous week’s decline.

Chinese retail sales and industrial production headline economic data being released this week. The Federal Reserve will release the minutes from its latest meeting. Given the big increase in U.S. consumer prices, similar data releases in the eurozone, the United Kingdom, and Japan will garner extra attention.

Figure 1

Economies in Low and High Places

Big entertainment events have struggled during COVID, but leave it to Garth Brooks to put a surge back into the entertainment industry. Rather than focus on large indoor concerts, Brooks decided mega-sized events at football stadiums were the way to go. The concerts will have fans in low and high places as they flock to buy seats. One stadium, which hadn’t hosted an event in 34 years, sold 70,000 tickets in 47 minutes.

World economies and markets are experiencing their own highs and lows. The two largest economies, the U.S. and China, are experiencing some of the strongest recoveries. The U.S. Purchasing Managers Index (PMI) shot to 68.1 and zoomed past expectations of 63.7. Services were the strongest segment, reaching 70.1 on a program that gauges what percentage of companies are experiencing an expansion or contraction. The data would have been better if not for supply shortages and difficulties finding labor.

China’s economy also is bouncing back from COVID. The country’s severe lockdown caused retail sales to crash 15% lower, when compared to the previous year. After bouncing back 34.2% in March from the worst lockdown period a year ago, April retail sales gained 17.7%. Expectations were for 25% growth, so the result indicated China’s consumers are not returning as quickly as some expected.

China’s industrial prowess remains impressive. Industrial production dropped much less during the lockdowns than it did in other countries; yet, it still managed to rally 9.8% last month.

European economies are also rallying compared to the peak of COVID restrictions from last year. British retail sales jumped 42.4% as the economy reopened. Clothing sales gained 70%. Europe’s ability to sustain an economic recovery and expand its vaccination program will likely play a key role in the ongoing recovery.

By contrast, the world’s third largest economy, Japan, is experiencing economic lows. Japan’s first-quarter GDP slipped 1.3% as private consumption sank 1.4%. Japan’s most pressing problem is a COVID surge that pushed new cases to a near record. An outbreak early in the fourth quarter led to increased new cases in January and a new lockdown. Another recent jump in cases created a similar response. As we have seen around the world, when economies limit mobility, economic activity declines.

What the data tell us is much of the global economy is bounding back when compared to the COVID lockdowns of 2020. As those lockdowns drop off the one-year data, growth moves lower. Any sustained recovery will need countries to open up additional activities in order to regain some jobs. Many eyes will be on Japan as it seeks to fill stadiums in late July and early August at the postponed 2020 Olympics. Hopefully, Japan will make rapid strides for the health of its citizens and for athletes and fans from around the world.

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.garthbrooks.com/performances

https://www.worldometers.info/coronavirus/country/japan/

https://www.cnbc.com/2021/05/17/china-economy-april-retail-sales.html

https://asia.nikkei.com/Economy/Japan-GDP-shrinks-annualized-5.1-in-Q1

https://www.reuters.com/business/retail-consumer/uk-retail-sales-jump-92-shops-reopen-2021-05-21/

https://www.dol.gov/ui/data.pdf

https://www.nar.realtor/newsroom/existing-home-sales-decline-2-7-in-april

Compliance Case #01040687